Throughput Accounting is a modern management accounting technique that offers an alternative view to the more traditional cost accounting.

It’s all about identifying the constraint or limiting factor in the production process and exploiting it to maximise profit. It allows management to focus efforts to make the best possible use of the limitation.

Theory of Constraints “TOC”

Goldratt’s Theory of Constrains is a methodology that is covered in the CIMA P2 syllabus and can be applied to systems that are unable to fulfil their goals or targets. Goldratt suggests that any process is only as strong as it’s weakest link and all effort should be focused on removing the constraint by following a five step process.

The constraint in a manufacturing environment is also referred to as a “bottleneck”

- Identity Constraint

- Decide how to exploit the constraint

- Sub ordinate other activities/non-constraints

- Elevate the constraint

- Repeat the process

These five steps ensure the organisation has an ongoing improvement that is based on the identified constraints or weak links.

And it’s measurements are given via Throughput Accounting – which Goldratt describes as key performance measure.

Throughput Accounting

Is also known as the rate at which the system generates money, it is measured in monetary terms and naturally linked to profitability. Therefore, the objective is achieve the maximum possible throughput profit or “flow”.

Throughput Accounting is based around achieving the maximum possible net profit in a limited time frame with limiting conditions. The formulas used and and a scenario based example is the best way to illustrate how Throughput Accounting can be used and the principles behind it.

Formula and Ratios

Throughput $ = Sales Revenue less Direct Material Costs

Throughput Accounting Ratio (TPAR) = Return per factory hour/Cost per factory hour

Return per factory hour = Throughput $ per unit/Time per unit

Cost per factory hour = Total factory cost/Total time available

The two key formulas here are the Throughput $ and the TPAR – the other formulas are required to understand how to calculate the TPAR.

Below is a scenario of limiting factors and how throughput accounting can be applied as how to maximise profit.

Production Plan to Maximise Profit

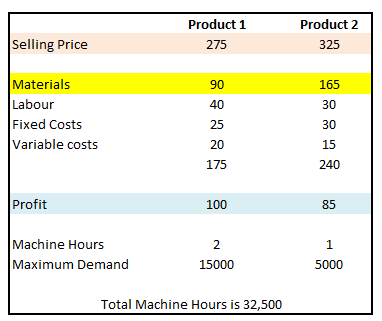

The TOC Theory of Constraints in this scenario is the fact the total machine hours is just 32,500 yet to fulfill the demand required we would need 35,000 hours (15,000*2)+(5000*1).

To calculate the production plan to achieve the maximum profit we need to find the Throughput value per machine hour, which we know is the Selling Price less the Materials/the total machine hours per unit.

Product A $175 (275-90)/2 hours = $92.50

Product B $125 (325-165)/1 hour = $160

With this mind, we need to exploit the constraint by maximising the production of Product B as it gives the highest throughput value and filling the rest of the time with Product A to achieve the maximum profit in these conditions.

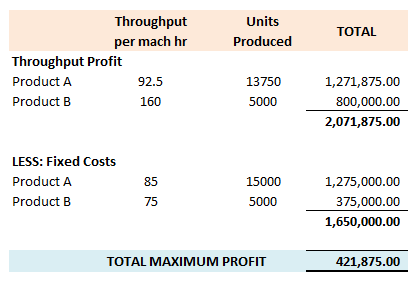

Proposed Production Plan

Product B: 5000 units x 1 hours = 5,000 machine hours

Product A: 13,750 units x 2 hours = 27,500 machine hours

Below is a summary of the financials based on this production plan.

You can see the total throughput profit (which is considering just the direct materials as a variable cost) gives over 2m profit.

However, the factory (or total fixed costs) need to considered and this is based on the number of units in the original demand and not the proposed production plan as the fixed costs will be incurred regardless of any constraint.

The final result would be a total maximum profit of 421,875.

TPAR – Throughput Accounting Ratio

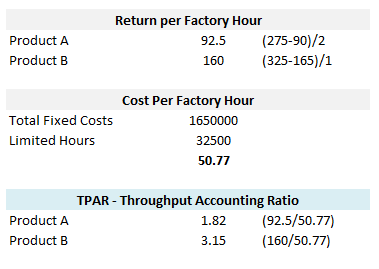

Finally, let’s look at the TPAR based on the above scenario and see what that tells us.

The TPAR ratio is calculated on each product and is done by dividing the Return Per Factory Hour against the Cost Per Factory.

You can see that both products have a ratio above 1 which means that the product will be profitable – in simple terms in means that the throughput profit is greater than the fixed costs. In fact you can see that Product B gives a TPAR of a whopping 3.15, so making over three times profit in relation to the fixed costs.

Leave a comment