The CIMA F1 Financial Reporting exam is not as tough as many students fear. I remember myself when studying for this paper I dreaded the accounting standards and technical elements of the paper. Fearing that I would never be able to remember and apply them on exam day.

Nevertheless, I did manage a first time pass with the F1 Financial Reporting paper, although this was back around 2014 when the exams were not computer based and the questions were in longer format. But the fundamentals and principles remain the same.

If you are one of the those students that are immediately filled with dread when opening your F1 Financial Reporting textbook (or pdf online text as is the case these days). Then fear not.

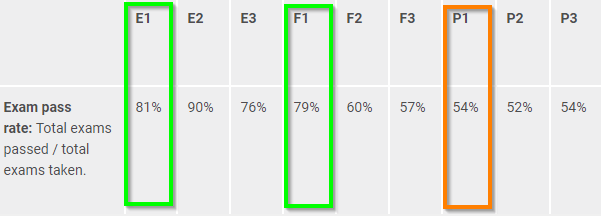

A quick glance at the CIMA Exam Pass Rates during 2020 paint a happy picture. The CIMA F1 paper had a 79% pass rate, while the E1 paper (which is considered one of the easier papers) had an 81% pass rate. If you should fear anything at this level it should be the P1 paper which had a very modest 54%.

The F1 Syllabus

F1: Financial Reporting

A. Regulatory environment of financial reporting

B. Financial statements

C. Principles of taxation

D. Managing cash and working capital

The area I want to focus on here is section D on the F1 syllabus: Managing Cash and Working Capital as it’s an area that can be tested heavily in both the objective tests and the case study at operational level.

Understanding Working Capital

Working capital is a measure of the company’s liquidity and is calculated by deducting the current liabilities (trade payables, overdraft etc.) from the current assets (inventory, cash and receivables).

Working Capital = Current Assets – Current Liabilities

It’s a simple formula that tells you how liquid the company is. Perhaps the best way to approach this subject to start from the end and break it down step by step.

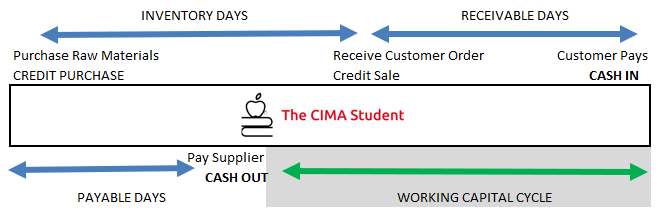

The Working Capital Cycle

Many companies will measure the working capital cycle to identify any areas of concern with how the company invests it’s cash. It can tell you if there is an issue with how long it takes to collect cash, are they not utilizing payment terms effectively and do they hold too much inventory?

Simply put;

it’s the length of time between paying suppliers for the purchase of raw materials and receiving cash back into the business when the customer pays our invoice.

The shorter this cycle is, the more efficient the company is run and the quick it can start the process again.

Here is an illustration of The Working Capital Cycle.

The focus will be on the green arrow – how can companies positively impact this cycle?

• Payable Days – is the company making full use of payment terms? This blue arrow could be pushed further out to shorten the working capital cycle.

• Receivable Days – is cash being collected on time? If not, what are the issues? Improving cash collection and reducing this blue arrow would help shorten the working capital cycle.

• Inventory Days – how long is the company holding onto inventory for, can sales be generated more efficiently and can the production process be quicker?

It’s more feasible for a company to focus on extending payment terms and improving cash collection rather than looking at the production or inventory process. These are the kind of questions and thought process you should be going through during a case study exam.

While the objective tests and specifically the F1 Financial Reporting paper you will be required to perform quick calculations and select the right answer.

Measuring Working Capital

These ratios are used to determine how much working capital a business holds and if it’s too much, or if there is a risk of the business not being liquid enough.

LIQUIDITY RATIOS

Current Ratio = Current Assets/Current Liabilities

In an ideal world, this should always be over 1.

This indicates the company holds more current assets than liabilities – in most industries the benchmark would be around 1.4 to 1.5. However, that is not always the case if we think about the Supermarket Industry where it’s common to be under 1.0.

This is due to the fact they have very little stock on hand as it’s fast moving and very little receivables due to customers paying cash in the store, this cash is used in a fast turnaround for more goods.

The Quick Ratio = Current Assets-Inventories/Current Liabilities

This removes inventory from the equation as it’s the least liquid. If there was an urgent need for a business to cover their liabilities in a short space, this measure will tell us if it’s possible.

It’s basically saying, do we have enough cash on hand and receivables to collect to pay all of our current liabilities. Ideally, it would be just over the 1.0 mark.

EFFICIENCY RATIOS

Inventory Days = Inventory/Cost of Sales x 365

This measure will tell us how long a company holds onto inventory before it’s sold. If this period is too long or increases over time, then the cost of storing the inventory grows and so does the risk of obsolescence.

Receivables Collection Period = Trade Receivables/Revenue x 365

Here we will understand how efficient the cash collection process is, if the company offers a strict 30 payment terms to their customers but this measure is well over 30 days, the company needs to address it. The shorter this period, the quicker the company can invest the money back into the production of goods and services.

Payables Payment Period = Trade Payables/Cost of Sales x 365

As above, but from other side. If the company has 60 day terms to pay their supplier bit this measure shows only 50 days, then there is a case of paying some suppliers too early. Alternatively, if there is a strain on the working capital cycle a company may look to negotiate longer payment terms with their suppliers.

The Working Capital Cycle = Inventory Days + Receivable Days – Payable Days

Now we can calculate the working capital cycle in days by adding the inventory days to the receivable days and deducting the payable days.

Let’s take a look at example illustrating these ratios in action.

The current ratio of 1.55 is very healthy and shows the company has plenty of current assets to cover their liabilities in the short term. However, if we take inventory out of the equation the quick ratio of 0.81 illustrates the company may struggle to meet their liabilities and need to think about their inventory management.

The Inventory Days of 112 is also high and backups up the quick ratio, that the company is holding too much inventory and for too long. If we look at it in pure values, there is 2000 worth of inventory on the balance sheet despite the cost of sales for the whole year is 6500.

On the other hand, the payable days look to be good. The company is taking 98 days to their creditors which is effective use of the company’s cash, although there needs to balance to ensure vendors are not being LATE and there is a risk of services being cut off.

The receivable days also look to be in good shape, 40 days to collect cash is a good measure but of course this can be benchmarked to their current receivable terms. Is it 30 days, 60 days? In a case study exam you will usually be given some context to judge these numbers on.

In terms of the F1 Financial Reporting objective test, practice calculating the ratios and there are various ways the working capital cycle can be tested. You might be given the ratios themselves and then asked to calculate the total payables value on the balance sheet, all of these type of questions will be most exam practice kits.

Leave a comment